By Alabama Center for Real Estate (ACRE)

Click here to view or print the entire November report compliments of the ACRE Corporate Cabinet.

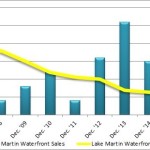

Lake Martin Area* residential sales totaled 30 units, an improvement in sales growth of 11.1 percent from the same period a year earlier. November sales were 1 unit below our monthly forecast. YTD sales are up 9.2 percent from 2013. The Center’s year-to-date sales forecast projected 428 closed transactions through November while the actual closings were 440 units representing a cumulative favorable variance of 2.8 percent.

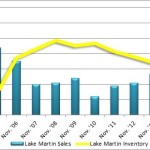

Supply: The Lake Martin Area housing inventory in October was 519 units, an increase of 5.9 percent from November 2013 but 20.8 percent below (this is good news) the month of November peak in 2008 (655 units). In contrast, October inventory decreased by 1.3 percent from the prior month. This direction is consistent with historical data indicating that October inventory on average (’09-’13) traditionally decreases from the month of October by 1.6 percent. There were 17.3 months of housing supply (8.5 months considered equilibrium in November NSA) in November, a decrease of 4.7 percent from last November’s 18.1 months of supply.

Demand: As anticipated, November residential sales slipped 26.8 percent from the prior month. This direction is consistent with seasonal buying patterns and historical data that indicates November sales, on average (’09-’13), typically decrease by 35.6 percent from the month of October.

Pricing: The Lake Martin Area median sales price in November was $161,000, a decrease of 40.4 percent from November 2013 and a 35.6 percent decrease compared to the prior month (such decrease is an anomaly & not sustainable). Historical data and seasonal trends indicate that the November median price (’09-’13) typically decreased by 19.5 percent from the month of October. Pricing can & will fluctuate from month-to-month due to changing composition of actual sales (lakefront vs non-lakefront) and as the sample size of data (closed transactions) is subject to seasonal buying patterns. A a broader lens as to pricing trends is appropriate and we highly recommend contacting a local real estate professional for additional market pricing information.

Industry Perspective: “November’s National Housing Survey results support the 2014 trend of gradual, but often sporadic and unspectacular, improvement across a range of indicators measuring consumer attitudes toward housing – mirroring the uneven recovery in housing activity this year,” said Doug Duncan, senior vice president and chief economist at Fannie Mae. “More encouraging is the steady upward trend this year in consumers’ assessment of their personal finances, with 46 percent of Americans – near the survey’s high – expecting their personal financial situation to improve over the next 12 months. We expect consumer attitudes toward housing to improve as the pickup in the overall economy lifts employment and income prospects. However, a sustained improvement in sentiment that could support a robust housing recovery, as policy support is removed, will require meaningful gains in household income. While such gains have so far been elusive, the strength in the November jobs report, which points to faster growth in labor income in the current quarter, marks a good start.” For full report, go HERE.